Florida Long-Term Care Partnership Program: A Comprehensive Guide

January 9, 2025

R. Gardner Sherrill MBA, CFP

connect with us

®

Personalized Financial Planning

For a confident retirement

Guiding Your Retirement Journey with Integrity & expertise

investing

post categories

economy

Executive Summary

The Florida Long-Term Care Partnership Program is a strategic collaboration between Florida Medicaid and private insurers. It is designed to address the growing demands of long-term care while protecting policyholder assets. This program enables individuals to secure their financial future through qualified long-term care insurance policies while maintaining Medicaid eligibility.

Program Overview

The Partnership Program, established in 2007, offers a dollar-for-dollar asset protection model. For every dollar a qualified long-term care insurance policy pays out, an equivalent amount of assets is protected from Medicaid spend-down requirements. This structure incentivizes private insurance acquisition while reducing state Medicaid expenditures.

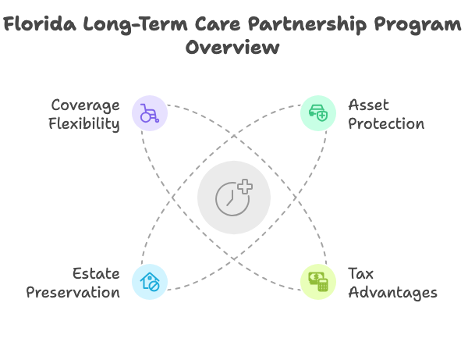

Key Benefits

- Asset Protection: Dollar-for-dollar asset protection against Medicaid spend-down requirements

- Tax Advantages: Premium payments may qualify for federal tax deductions

- Estate Preservation: Protected assets remain exempt from Medicaid estate recovery

- Coverage Flexibility: Policies cover various care settings, including home care, assisted living, and nursing facilities

Eligibility Requirements

- Purchase of a Partnership-qualified long-term care insurance policy

- The policy must include inflation protection (exemption for ages 75+)

- Medicaid approval is required for asset protection benefits

- The policy must meet tax qualification standards under federal law

Financial Planning Considerations

The program requires strategic financial planning, particularly regarding:

- Premium costs vary by location and coverage level

- Asset protection strategies aligning with estate planning goals

- Integration with existing retirement and healthcare planning

- Consideration of inflation protection requirements

Legal Framework

The program operates under Florida Statute 409.9102, with specific requirements outlined in Florida Administrative Code Chapter 69O-157.201. These regulations ensure consumer protection and program integrity while complying with federal guidelines.

Implementation Process

- Research qualified insurance providers

- Select appropriate coverage levels and options

- Verify Partnership Program qualification

- Maintain documentation for future Medicaid applications

Provider Selection

When selecting a provider, evaluate:

- Financial stability ratings

- Claims payment history

- Customer service quality

- Premium stability track record

- Partnership Program certification

Cost Management

Long-term care costs in Florida vary significantly by region and service type. Daily costs typically range from $100 to $250, emphasizing the importance of adequate coverage selection and inflation protection.

Professional Guidance

Consultation with qualified financial planners and legal professionals ensures:

- Appropriate coverage selection

- Integration with existing estate plans

- Maximum tax benefit utilization

- Optimal asset protection strategies

Future Considerations

The program’s importance continues to grow with:

- Increasing healthcare costs

- Aging population demographics

- Rising long-term care service demands

- Evolving Medicaid regulations

Contact Information

For detailed program information:

- Florida Department of Elder Affairs

- Agency for Health Care Administration

- Office of Insurance Regulation

This guide is foundational for understanding the Florida Long-Term Care Partnership Program. Individuals should consult qualified professionals for specific advice regarding their circumstances.

As the population ages, long-term care becomes increasingly vital, particularly in sunny Florida, where retirees flock for its inviting climate. Long-term care encompasses a range of services designed to support individuals with chronic health issues or disabilities, highlighting the importance of understanding the options available. Amidst rising healthcare costs, the Florida Long-Term Care Partnership Program offers a unique solution for those planning for their future needs.

This program offers individuals the chance to protect their assets while receiving necessary care and plays a critical role in determining Medicaid eligibility. With a variety of coverage options and financial benefits, it’s crucial to explore how the partnership functions and the advantages it can provide to residents. Grasping the essential components of the program can empower Floridians to make informed choices regarding their long-term care plans.

In this comprehensive guide, we will examine the details of the Florida Long-Term Care Partnership Program, covering eligibility requirements and key features of long-term care insurance. We will also clarify common misconceptions, outline the application process, and offer insights into how financial planners can help navigate this vital aspect of healthcare planning.

Overview of Long-Term Care in Florida

Florida’s Long-Term Care Partnership Program encourages the purchase of private long-term care insurance. This program, a partnership between Medicaid and private insurers, offers dollar-for-dollar asset protection. That is, each dollar spent on private insurance protects a dollar of assets. This can be important when applying for Medicaid assistance.

Key points about the program include:

– Tax-Qualified Policies: Insurance policies must be tax-qualified.

– Inflation Protection: Policies must offer inflation protection. Requirements vary by age.

– Financial Relief: Aims to reduce financial burdens of long-term care.

– Established in 2007: Helps alleviate costs associated with nursing facilities and other services.

| Senior Population in Florida | Need for Long-Term Care |

| Nearly 3.4 million aged 65+ | Growing economic challenges |

The program began in 2007. It was created due to the growing need for long-term care, as Florida’s senior population increases. Elderly residents hit 3.4 million, emphasizing the challenges families and Medicaid face. With the partnership program, individuals can better protect their assets while managing long-term care needs.

Benefits of the Florida Long-Term Care Partnership Program

The Florida Long-Term Care Partnership Program offers several key benefits for residents planning for future care needs. Here are the main advantages:

- Proactive Planning: Encourages buying private long-term care insurance to reduce financial strain associated with care services.

- Dollar-for-Dollar Asset Protection: For every dollar in benefits paid by the insurance, an equal amount of assets is protected from Medicaid’s spend-down rules.

- Tax Deductions: These policies are tax-qualified, allowing policyholders to deduct part of their premium payments under federal law.

- Financial Risk Mitigation: Shifts the initial care costs to private insurers, with the state providing backup for extended care needs.

- Protecting Savings: By participating, individuals can safeguard their assets from high expenses like nursing homes, assisted living, or home health care.

In summary, the Florida Long-Term Care Partnership Program helps residents plan by integrating private insurance with state support. This proactive approach protects assets and reduces financial risks in long-term care scenarios.

Eligibility Requirements for the Partnership Program

The Florida Long-Term Care Partnership Program offers unique benefits for those planning for future care needs. To be eligible, you must purchase a partnership-eligible long-term care insurance policy while in good health. This policy must be tax-qualified, allowing some costs to be tax-deductible.

Key Requirements:

Inflation Protection: Policies must include inflation protection to keep up with rising care costs. However, individuals over 75 are exempt from this requirement.

– Medicaid Approval: To receive asset protection benefits, policyholders must be approved for Medicaid Long-Term Care services in Florida or a state with a reciprocal agreement.

One notable advantage of this program is asset protection. Under the program, you can protect an amount of personal assets equal to what the insurance policy has paid. This is particularly helpful when applying for Medicaid after your long-term care benefits are used up.

The policy’s tax benefits, asset disregard, and protection from estate recovery make it a compelling choice for long-term financial planning. To fully benefit from the Florida Long-Term Care Partnership Program, ensure that your policy meets these criteria.

Key Features of Long-Term Care Insurance

Long-term care insurance provides quality care at home, in nursing homes, adult daycare, or assisted living facilities. However, it usually does not cover housing costs in these settings. Policies are flexible and tailored to meet the policyholder’s needs and desired coverage. In Florida, there is no standardization, meaning that coverage options and pricing can vary greatly among different policies.

Key features of long-term care insurance include:

- Customized Benefits: Choose the amount and type of care needed.

- Asset Protection: Partnership policies protect assets from Medicaid spend-down requirements, equal to benefits paid.

- Support for Daily Activities: This program offers financial assistance to those who are unable to perform daily tasks due to disability or infirmity.

- Range of Services: Covers medical, personal, and social services.

| Feature | Description |

| Customized Benefits | Tailors coverage to individual needs |

| Asset Protection | Shields equivalent assets from Medicaid rules |

| Daily Activities | Financial aid for personal care |

By providing this support, long-term care insurance offers peace of mind for future healthcare needs.

Popular Long-Term Care Insurance Providers in Florida

Florida’s Long-Term Care Partnership Program encourages residents to purchase private long-term care insurance. This program offers dollar-for-dollar asset protection. It makes it easier for policyholders to integrate their insurance with Medicaid for better asset protection. Many of these policies are partnership-certified in Florida.

Long-term care insurance helps cover costs associated with nursing homes, in-home care, and assisted living, which are often not covered by regular health insurance or Medicaid. Florida’s partnership program also includes tax-qualified policies, which means policyholders can claim part of their premiums as a tax deduction.

Popular Long-Term Care Insurance Providers in Florida

Here are some of the popular providers offering partnership policies in Florida:

- Genworth Financial

– Offers comprehensive care plans.

– Known for flexible benefits. - Mutual of Omaha

– Provides a range of customization options.

– Strong customer service reputation. - New York Life

– Features inflation protection to safeguard benefits.

– Offers joint policies for couples.

These providers help Floridians secure their financial future while meeting Medicaid spend-down requirements. By choosing partnership policies, residents can protect a dollar of assets for every dollar their insurance pays out on their behalf.

Understanding Premium Costs for Long-Term Care

Understanding the costs of long-term care is essential for future planning. In Florida, the premiums for long-term care insurance vary by location. For instance, daily costs can range from $100 to $250, depending on the city you live in.

The Florida Long-Term Care Partnership Program encourages buying private insurance. This helps manage the high costs of long-term care services. With partnership policies, you can protect assets equal to the benefits paid out. This ensures you won’t need to deplete your savings to qualify for Medicaid.

Key Features of Partnership Policies:

– Custom Design: Choose the level of benefits you want.

– Inflation Protection: Keep up with rising costs.

– Asset Protection: Avoid Medicaid spend-down requirements.

Each policyholder can tailor their coverage. This customization affects premium costs. The more benefits you choose, the higher the premium.

In summary, Florida’s Long-Term Care Partnership Program offers a way to safeguard your financial future while managing long-term care expenses.

Asset Protection Strategies through the Partnership Program

The Florida Long-Term Care Partnership Program helps Medicaid applicants with long-term care insurance protect their assets. Typically, people must spend most of their assets before qualifying for Medicaid coverage. However, with a Partnership policy, policyholders earn dollar-for-dollar asset disregards. This means for every dollar the insurance pays, you can protect the same amount of assets.

For example, if your policy covers $300,000 in care, you can keep $300,000 in assets when applying for Medicaid. This protection shields assets from Medicaid’s spend-down requirements and Medicaid Estate Recovery. Estate Recovery normally seeks to reclaim costs from a deceased person’s estate. But with this program, you can pass your wealth to heirs.

Asset Protection Benefits of the Florida Partnership Program:

- Dollar-for-Dollar Asset Disregard: Protects the same amount of assets as your policy payout.

- Exemption from Medicaid Spend-Down: Retain more wealth while qualifying for assistance.

- Protection from Estate Recovery: Easier wealth transfer to heirs.

The program encourages purchasing private long-term care insurance. These policies offer strategies that help you plan for future care needs while keeping more of your assets.

How the Partnership Program Affects Medicaid Eligibility

The Florida Long-Term Care Partnership Program impacts Medicaid eligibility by allowing individuals to maintain some assets while accessing long-term care benefits. Under this program, for every dollar paid by a Partnership Long-Term Care Insurance policy, an equal dollar of assets is protected from Medicaid’s spend-down requirements. This feature enhances asset protection, which is key to safeguarding financial security.

List of Key Benefits:

– Dollar-for-Dollar Asset Protection: Helps individuals keep wealth intact.

– Medicaid Spend-Down Protection: Protects assets equivalent to insurance payouts.

– Estate Recovery Shielding: Assets protected are exempt from Medicaid’s recovery after death.

The program also encourages purchasing private long-term care insurance. By providing dollar-for-dollar asset protection, individuals are incentivized to invest in these policies. It helps them preserve their financial legacy.

To maximize benefits, it’s crucial to purchase a Partnership Program policy while in good health. This improves eligibility and aligns long-term care needs with financial security. By participating, individuals can protect their estate and ensure coverage in times of need.

Legal Framework: Florida Statutes and Regulations

The Florida Long-Term Care Partnership Program was established under section 409.9102 of the Florida Statutes. This initiative forms a partnership between Medicaid and private long-term care insurers. It is designed to help residents afford long-term care without depleting their savings.

The Florida Administrative Code Chapter 69O-157.201 sets the standards for these policies. It ensures that all insurers comply with state regulations. The program is a joint effort involving multiple agencies. These include the Agency for Health Care Administration, the Office of Insurance Regulation, and the Department of Children and Family Services.

Here’s a quick overview of relevant legislation:

- Chapter 627.94075

– Defines scope, rates, and contracts for the program. - Tax Benefits

– Policies offer tax-qualified benefits.

– Premiums paid can be claimed as a tax deduction under federal law.

By allowing policyholders to protect their assets, this program offers peace of mind and financial relief. It also aids in meeting Medicaid spend-down requirements, providing a safeguard against estate recovery.

Application Process for the Partnership Program

The application process for Florida’s Long-Term Care Partnership Program is straightforward. To enroll, residents must first purchase a qualifying Long-Term Care Insurance policy. These policies must meet specific criteria set by the program.

Here’s a simple list of steps to follow:

- Research: Find private insurers participating in the program. Make sure they offer policies that qualify under Florida’s guidelines.

- Purchase: Choose and purchase a policy that includes inflation protection, which is a requirement.

- Verify: Confirm with your insurer that your policy qualifies under the Florida Partnership rules. This ensures eligibility for the asset protection benefits.

Once a qualifying policy is in place, policyholders can enjoy dollar-for-dollar asset protection. For every dollar the insurance pays, it protects an equal amount of the policyholder’s assets. This protection comes into play if individuals need Medicaid long-term care services. It allows them to access Medicaid benefits without first spending down their assets.

The program is part of a partnership between Florida’s Medicaid program and private insurers, inspired by the Deficit Reduction Act of 2006. This collaboration means residents have more control over their financial future while covering long-term care costs.

Comparing Long-Term Care Coverage Options

When comparing long-term care coverage options, understanding your choices is crucial. Long-term care insurance policies cover care in places like home care and nursing homes. However, they usually don’t cover housing costs. In Florida, the Long-Term Care Partnership Program encourages buying private long-term care insurance. It offers dollar-for-dollar asset protection, which means you can protect assets equal to the benefits you get from the insurance.

Here is an overview of the program:

– Asset Protection: Safeguards assets linked to the benefits received.

– Medicaid Eligibility: Easier access due to protected assets.

Long-term care insurance options in Florida vary. There’s no set standard, so coverage and costs differ among providers.

Tips for Choosing Coverage:

– Start looking for coverage early, especially if you’re over 50.

– Health issues might increase premiums over time.

Finding the right policy means matching your needs with what’s available. Studying and comparing options can help you select a suitable plan for your long-term care needs.

Critical Considerations Before Enrolling in the Program

Before enrolling in Florida’s Long-Term Care Partnership Program, consider several critical points:

- Dollar-for-Dollar Asset Protection: This feature allows policyholders to protect more assets when qualifying for Medicaid. You can keep an equivalent amount in assets for every dollar your insurance policy pays.

- Tax Deduction Benefits: These policies are tax-qualified, meaning a portion of your premiums might be tax-deductible. This can provide a substantial financial advantage.

- State Reciprocity: Not all states recognize out-of-state partnership policies for Medicaid. However, Florida honors policies from states with reciprocal agreements.

- Eligibility Thresholds: The program allows you to hold assets that match the benefits paid by your policy, exceeding the usual Medicaid asset cap of $2,000.

- Inflation Protection: Make sure your policy includes inflation protection to maintain its value over time.

To maximize the benefits of the Long-Term Care Partnership Program, keep these considerations in mind. Balancing immediate costs with long-term gains is essential for effective financial planning.

The Role of Financial Planners in Long-Term Care

Financial planners play a crucial role in long-term care planning. However, if they are employed by insurance companies, they might face conflicts of interest, which could lead to less transparency when advising on long-term care options.

Key Points:

Independent agents can offer personalized service without the bias of company ties. They focus on finding the best policies for clients’ needs.

– Specialists’ Assistance: A knowledgeable long-term care specialist helps clients navigate options and choose the right insurance policy.

– Retirement Planning Tool: Long-term care insurance is vital in protecting savings and assets if care services are needed.

Financial planners must understand the link between state Medicaid programs and private insurers. This partnership can affect clients’ financial strategies for long-term care. Knowing about Medicaid’s dollar asset protection and spend-down requirements is essential. These insights help clients maximize their resources while planning for their future.

Remember:

– Check if the planner is independent or tied to an insurance company.

– Discover if policies include inflation protection or estate recovery options.

– Consider the planner’s awareness of policy benefits like tax deductions.

Policyholders can better prepare for long-term care costs and protect their assets by choosing the right financial planner.

Understanding the Growing Costs of Long-Term Healthcare

Florida faces rising long-term healthcare costs. This is due to higher demand, increased labor costs, and inflation. The aging population and retirees moving to Florida add pressure.

As people age, the risk of needing long-term care increases. Many older residents struggle with long-term care expenses, which can quickly drain their income and assets.

Long-term Care Insurance offers financial support. It helps policyholders manage potential resource depletion.

To address this, Florida’s Long-Term Care Partnership Program offers a solution. This program allows seniors to keep more assets than traditional Medicaid, helping them better manage their finances while receiving care.

Here’s a quick look at the factors contributing to rising costs:

– Growing aging population

– Increased demand for care

– Higher labor costs

– Inflation

– Influx of retirees

Long-term care planning is crucial in managing these rising costs and ensuring financial stability in later years.

Tax Incentives Related to Long-Term Care Insurance

Florida’s Long-Term Care Partnership Program offers significant tax incentives for those purchasing long-term care insurance policies. These policies are federally tax-qualified, meaning you can deduct part or all of the premiums from your federal income tax. This tax deduction can make long-term care coverage more affordable and appealing.

Key Tax Advantages

– Tax Deductions: Premiums for qualified policies can be partially or fully deducted from federal income taxes.

– Proactive Planning Incentive: The potential tax savings encourage individuals to plan for future health care needs.

Older policies, mainly those sold before 1992, may require hospitalization, reflecting changes in eligibility criteria for tax benefits over time.

Summary Table

| Tax Benefit | Details |

| Federal Tax Deduction | Deduct premiums from federal taxes. |

| Encourages Early Planning | Incentivizes securing coverage early. |

| Enhanced Affordability | Makes policies more financially accessible. |

These tax incentives are a compelling reason to consider long-term care insurance as part of your financial planning strategy. By taking advantage of these benefits, you can better manage care costs in the future.

Common Misconceptions About Long-Term Care Insurance

Long-term care insurance is frequently misunderstood. Many people believe it only covers nursing home care. In reality, numerous policies also assist with care at home or in assisted living facilities. Here are some widespread misconceptions:

- Standardization: These policies are not one-size-fits-all. Each insurance company provides distinct benefits and terms, so it’s important to read the details of a policy carefully.

- Income Levels: Some believe that long-term care insurance is not beneficial for individuals with low income. However, a Partnership Long-Term Care Insurance policy enables you to retain more of your assets while qualifying for Medicaid benefits.

- Timing: Many wait to buy insurance until they need care. This is risky. Pre-existing conditions can increase costs or make you ineligible.

- Plan Necessity: People often underestimate the need for long-term care planning. However, the likelihood of needing long-term care services rises as we age.

Grasping these points can aid in making informed decisions regarding long-term care insurance. Keep in mind that planning ahead is essential for effectively managing future healthcare needs.

FAQs

What is the Florida Long-Term Care Partnership Program?

The Florida Long-Term Care Partnership Program is a collaboration between Medicaid and private long-term care insurers. It encourages people to purchase private long-term care insurance. This program offers tax-qualified policies. Policyholders can claim a portion of their premiums as a federal tax deduction. A key benefit is dollar-for-dollar asset protection. For every dollar paid out in benefits, a dollar of assets is protected from Medicaid spend-down requirements. Established in 2005, this program helps individuals secure their assets. It allows them to benefit from both private insurance and Medicaid.

How does the Partnership Program protect assets?

The Partnership Program assists individuals in retaining more of their assets when applying for Medicaid. For every dollar paid out by a Partnership-approved insurance policy, you can retain an equal amount in assets. This protection is applicable during Medicaid eligibility and also shields assets from Medicaid estate recovery after a policyholder’s death. Individuals with these policies can access Medicaid without significantly reducing their assets. This ensures financial security and safeguards family inheritances while receiving necessary care.

Are there limits on the benefits I can receive?

Long-term care insurance policies assist with costs related to daily living activities. The benefits of Partnership policies can increase with inflation, although some seniors may be exempt from this stipulation. To obtain asset protection benefits, you must be approved for Medicaid in the state where the policy is purchased. Ensure you are in relatively good health when purchasing your policy to maintain eligibility for when you need benefits.

Can I use the Partnership Program outside of Florida?

Florida’s Partnership Program acknowledges policies from reciprocal states, which is beneficial for residents considering a move. When relocating, it’s important to consult the new state’s Medicaid agency to verify participation. Not all states are involved in the program, which could affect benefits outside of Florida. Each dollar covered by your insurance policy allows you to retain a dollar in assets. However, states that are not part of the initiative may not recognize Florida’s asset protection.

What happens if I don’t use my long-term care insurance?

Not using your insurance could result in relying on Medicaid. Medicaid requires having minimal income and assets, which might lead to financial loss. You might need to spend down your assets to qualify, affecting your family’s inheritance. Without insurance, family members may face a financial burden to cover care costs. Insurance not used means missing out on asset protection, impacting estate preservation for heirs.

How do I choose the right long-term care insurance policy?

When choosing a policy, consider the daily benefit, maximum benefit period, and elimination period, as these factors influence coverage and costs. Purchase insurance in your fifties or sixties when premiums are generally lower. Select policies covering different care types, including at-home and nursing home care. Be aware of any hospitalization requirements for claim eligibility since some insurers may mandate it. Elect for a Partnership policy to secure additional asset protection when applying for Medicaid.

What is the Florida Long-Term Care Partnership Program?

The Florida Long-Term Care Partnership Program is a collaboration between Medicaid and private long-term care insurance companies. It encourages individuals to purchase private long-term care insurance policies. These policies are tax-qualified, meaning policyholders can claim part of their premiums as a federal tax deduction.

A standout feature of this program is dollar-for-dollar asset protection. For every dollar the insurance policy pays in benefits, an equal dollar in assets is shielded from Medicaid spend-down requirements. This means participants can protect their assets while still qualifying for Medicaid long-term care services.

Here’s a quick summary:

| Features | Benefits |

| Tax-Qualified Policies | Federal tax deductions for policyholders |

| Dollar-for-Dollar Asset Protection | Protects assets equivalent to insurance payouts |

| Access to Medicaid Benefits | No need to spend down income and assets to qualify for Medicaid services |

Approved by Florida’s legislature in 2005, the program started on January 1, 2007. It helps people secure their financial future, allowing them to retain more of their estate. By owning a Partnership policy, individuals can gain access to Medicaid long-term care benefits without stringent income or asset limitations.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.

Personalized Financial Planning, for a a confident retirement, based in Bradenton, FL - Serving clients across the US | Guiding your retirement with integrity and expertise.

Quick Contact Info

2520 Manatee Avenue West

Suite 200

Bradenton, FL 34205

info@sherrillwealth.com

941-745-2201

Site Menu

Site Menu

Our Services

Retirement Planning

Investment Management

Social Security Timing

Retirement Income

Tax Planning

Insurance Optimization

Estate and Legacy Planning

Retirement Readiness Masterclass

TO TOP

Advisory services offered through Commonwealth Financial Network®, a Registered Investment Advisor.

Information presented on this site is for informational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any product or security.

Certified Financial Planner Board of Standards

Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® (with plaque design) in the United States to Certified Financial Planner Board of Standards, Inc., which authorizes individuals who successfully complete the organization’s initial and ongoing certification requirements to use the certification mark.

This communication is strictly intended for individuals residing in the United States.

© 2012-2024 Sherrill Wealth Management | Privacy Policy | site credits

© 2012-2024 Sherrill Wealth Management

PRIVACY POLICY | site credits